- Tokenized

- Posts

- Why Everyone Wants to Be a Bank Again

Why Everyone Wants to Be a Bank Again

AND... Airwallex launches a stablecoin team, and House Republicans declare ‘Crypto Week’

Simon Taylor & Jeremy Batchelder

July 09, 2025

If you're reading this and still haven't signed up, click the subscribe button below!

Introduction

Welcome to the Tokenized newsletter, brought to you by the creators of the Tokenized Podcast; Simon Taylor of Fintech Brainfood and Pet Berisha of Sporting Crypto, written by Jeremy Batchelder.

We are the newsletter for institutions that need help preparing for a Tokenized future.

We run through the headlines every week, what it means for you and a market readout. Always with an institutional, business-focused perspective.

Join us every week as we meet your Tokenization needs.

Stories You Can't Miss 📰

🚀 Airwallex Builds Stablecoin Team Despite CEO's Apparent Skepticism

Visa-backed payments unicorn Airwallex is quietly building a major stablecoin operation, posting 22 stablecoin-related job openings despite CEO Jack Zhang's recent public skepticism about digital currencies for cross-border payments.

Key Points:

Airwallex is valued at $6.2 billion with $720M in annualized revenues and expects to surpass $1B in 2025, processing $130B in payments annually

The company recently posted 22 stablecoin job listings, signaling major infrastructure investment despite Zhang's public reservations

He acknowledged stablecoin utility for exotic currencies with poor liquidity and regulatory arbitrage opportunities in LATAM and Africa

Zhang's follow-up clarified his vision: stablecoins as "native money of the internet" rather than just payment rails

The Tokenized Take:

Classic misdirection play: Zhang's public skepticism about cross-border use cases may have been strategic positioning while Airwallex quietly builds stablecoin infrastructure for the "internet money" thesis

Distribution advantage recognized: Zhang argued that only established platforms like Airwallex, Stripe, and Revolut have the infrastructure to prove money is "clean" and achieve real adoption

Beyond payments focus: The hiring spree suggests Airwallex is building for stablecoin cards, money market funds, and lending products—not just cross-border transfers

Regulatory arbitrage timing: Airwallex is positioning to capitalize on regulatory differences between markets, particularly in emerging economies where traditional rails are weaker

Ecosystem monetization: Zhang sees the business model in card interchange fees and interest income from converting existing platform money into programmable stablecoins

🏛️ House Republicans Declare "Crypto Week" for Industry-Backed Bills

House Republicans are preparing to vote on three major cryptocurrency bills next week, including the bipartisan Genius Act that already passed the Senate 68-30, as they deliver on Trump's promise to end the Democrats' "crypto crackdown."

Key Points:

The Genius Act creates a regulatory framework for stablecoins, requiring issuers to register, hold reserves, and file disclosures while clarifying that stablecoins are not securities

The Clarity Act would establish "market structure" oversight, dividing responsibilities between the SEC and CFTC for cryptocurrency regulation

The anti-CBDC Surveillance State Act would permanently bar the federal government from issuing its own central bank digital currency

Trump personally intervened to push House Republicans to pass the Senate's Genius Act version rather than risk changes that could derail passage

At least one bill appears certain to become law, with the Genius Act having already secured bipartisan Senate support

The Tokenized Take:

Regulatory clarity finally arriving: After four years of enforcement-heavy approach under Biden's SEC, the industry gets the lighter regulatory framework it's long demanded

Stablecoin issuers are the big winners: By clarifying stablecoins aren't securities, issuers can keep investment returns on backing assets without strict disclosure requirements

Strategic timing advantage: Trump's crypto coin launch and exclusive investor dinners demonstrate the administration's commitment to industry-friendly policies

Market structure matters more than headlines: The Clarity Act's SEC/CFTC division of oversight could be more impactful long-term than the headline-grabbing anti-CBDC bill

Consumer protection trade-offs: Critics argue the bills grant "special treatment" by exempting crypto from traditional financial regulations while accessing government safety nets

💸 Stablecorner ⚖️ → The Banking Charter Arms Race: Why Everyone Wants to Be a Bank Again

The crypto industry spent over a decade criticizing traditional banking as outdated and extractive. Yet every major crypto company is now racing to become... a bank. As Joao Reginatto from M^0 candidly observed:

"A lot of us in crypto are in the business of critiquing banks and saying that is an outdated model, potentially an extractive model... But because of what's happening with genius, I think there's going to be a race now."

This banking charter gold rush reveals a fundamental truth: despite all the innovation, regulatory moats still determine who wins.

The Federal Charter Advantage

Circle's pursuit of becoming "First National Digital Currency Bank" isn't about prestige—it's about accessing critical infrastructure. Federal charters provide direct access to Fedmaster accounts and Fedwire, enabling stablecoin issuers to clear digital dollars without intermediaries.

Ripple and Anchorage Digital follow the same logic. These charters create "regulatory moat" advantages that become increasingly valuable as the industry scales, while also addressing the SVB lesson: concentration risk in traditional banking relationships poses systemic threats to the entire stablecoin ecosystem.

The Two-Tier Future

What's emerging is a clear bifurcation:

Tier 1: The Federal Champions - Circle, Ripple, and other chartered entities will dominate large institutional use cases requiring maximum regulatory compliance.

Tier 2: The Innovation Layer - The "long tail of fintech" building on composable infrastructure will serve thousands of new companies that can't access these large incumbents.

This creates a fascinating paradox: while crypto promised to eliminate intermediaries, it's actually creating more intermediaries than ever. But these serve as infrastructure providers enabling innovation rather than gatekeepers preventing it.

Why This Matters

The banking charter race isn't just competitive positioning—it's about defining the infrastructure layer for tokenized finance. The winners won't reject traditional banking entirely, nor simply recreate it with blockchain buzzwords. They'll use federal charters strategically: as infrastructure advantages that enable innovation rather than constraints that prevent it.

The great irony of crypto's evolution is that after spending years trying to eliminate banks, the industry's most successful companies are now racing to become them. But this time, they're building banks designed for a tokenized world—and that makes all the difference.

📰 Some More News:

🏦 Tokenization, Stablecoins & Finance

Bernstein says an 'equity tokenization wave' is coming, despite the Robinhood–OpenAI controversy (Read more here)

Ripple’s RLUSD Stablecoin to Power Cross-Margin Trading at Hidden Road, Brad Garlinghouse Confirms (Read more here)

SocGen Chair, ex ECB board member urges EU to embrace stablecoins (Read more here)

JD.com, Ant Group Push for Yuan-Based Stablecoins to Counter Dollar Rule: Reuters (Read more here)

Russian State Giant Rostec Plans Ruble-Pegged Stablecoin, Payment Platform on Tron (Read more here)

Solana and Fireblocks Selected by Japan’s Minna Bank for Stablecoin Use Case Study (Read more here)

🤑 Funding and M&A

💼 Government & Policy

Stand with Crypto joins over 60 other groups in urging US lawmakers to back sweeping crypto legislation (Read more here)

Korea’s central bank lobbies for further role in stablecoin oversight (Read more here)

Senate Revives Crypto Market Structure Efforts as House Prepares for Policy Votes (Read more here)

Bank of England eyes stablecoins for wholesale payments, tokenization (Read more here)

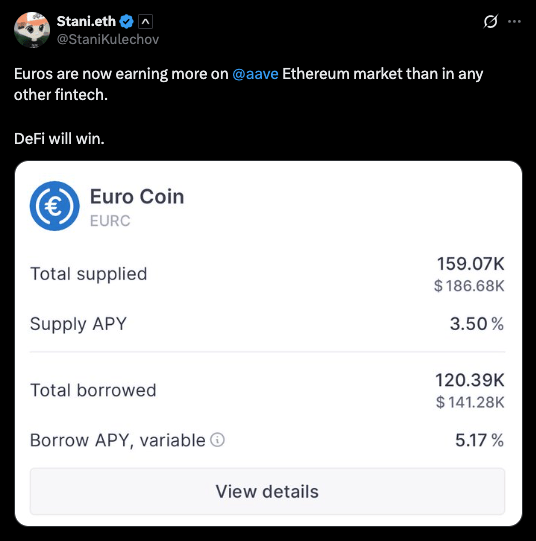

Tweet of the Week 🐤

From Stani Kulechov

Thanks so much for reading the Tokenized Newsletter!

Please share this edition or share it with your colleagues if you enjoyed it!

Disclaimers

This newsletter is for informational purposes only and is not financial, business or legal advice. These thoughts & opinions and do not represent the opinions of any other person, business, entity or sponsor. Any companies or projects mentioned are for illustrative purposes unless specified.

The contents of this newsletter should not be used in any public or private domain without the express permission of the author.

The contents of this newsletter should not be used for any commercial activity, for example - research report, consultancy activity, or paywalled article without the express permission of the author.

Please note, the services and products advertised by our sponsors (by use of terminology such as but not limited to; supported by, sponsored by, Made Possible by or brought to you by) in this newsletter could carry inherent risks and should not be regarded as completely safe or risk-free. Third-party entities provide these services and products, and we do not control, endorse, or guarantee the accuracy, efficacy, or safety of their offerings.

It's crucial to provide our readers with clear information regarding the inherent nature of services and products that might be covered in this newsletter, including those advertised by our sponsors from time to time. When you buy cryptoassets (including NFTs) your capital is at risk. Risks associated with cryptoassets include price volatility, loss of capital (the value of your cryptoassets could drop to zero), complexity, lack of regulation and lack of protection. Most service providers operating in the cryptoasset industry do not currently operate in a regulated industry. Therefore, please be aware that when you buy cryptoassets, you are not protected under financial compensation schemes and protections typically afforded to investors when dealing with regulated and authorised entities to operate as financial services firm.